February 2021: UK and Glasgow Economic and Rental Market Update

Last updated: 5.29pm, Monday 15th February 2021

We share important updates on the UK and Glasgow economy and detail on the current and forcasted rental market.

by Gordon Campbell

15th February 2021

COVID Update

The UK is still in a lockdown.

The number of new reported cases and fatalities have been reducing steadily thankfully.

Non-essential shops are closed.

Most businesses are open as usual.

Construction sector and related businesses is business as usual.

For Alliance Property Group it is business as usual.

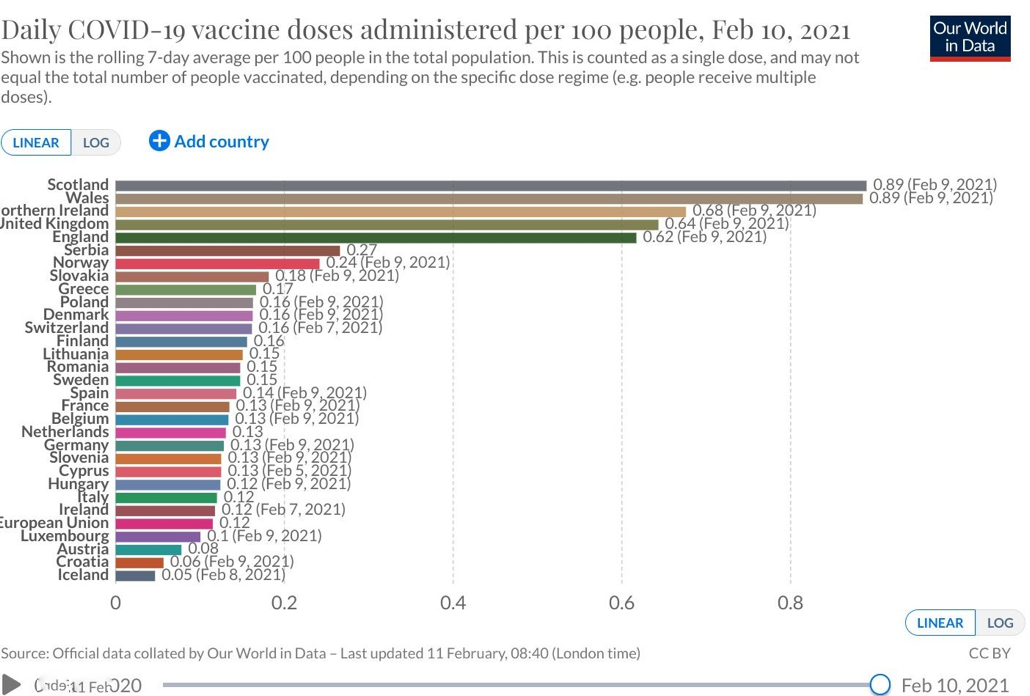

Vaccines

The vaccines roll out in the UK is successful and continues to be ramped up.

As of today, 15th February 2021, there is nearly 16m been vaccinated in the UK.

That will bring, without doubt, more confidence in the UK getting back to normality soon and the UK Prime Minister will announce forward plans this coming week.

UK Economy

The Bank of England has forecast a rapid recovery for the economy as vaccines are rolled out - but downgraded its growth outlook for the year as a whole.

GDP is expected to shrink by around 4% in the current first quarter, holding back Britain's recovery from the coronavirus crisis, as a result of latest lockdown measures.

That will drag on growth for 2021 as a whole, which the Bank forecasts will be just 5%, compared to a previously-predicted 7.25%.

But the quarterly monetary policy report suggests a sunnier outlook for much of the rest of the year.

"GDP is projected to recover rapidly towards pre-COVID levels over 2021, as the vaccination programme is assumed to lead to an easing of COVID-related restrictions and people's health concerns," it said.

For 2022, the Bank predicts growth of 7.25%, up from a previously forecast 6.25%.

The Bank noted that the recovery in spending could be stronger if consumers who have built up savings during lockdowns splash out more than current projections - which suggest they will only burn through 5% of them.

Data suggests that between March and November last year, households stashed away over £125bn more than they usually would, and will have accumulated even more since then.

"The current environment is clearly highly unusual historically, and there are reasons to think that households may choose to spend more of their recently accumulated savings," the Bank said.

Overall, the Bank said, COVID-19 will weigh more heavily on the economy than it had been expected to in previous forecasts made in November.

The Bank still expects that unemployment will peak at 7.75% later this year and that GDP will return to pre-COVID levels early next year.

Brexit

Life continues. No problems. No economic ceilings coming in.

Yes, there has been a few teething problems including at Dover Port but that is all now resolved and goods are flowing freely.

I am sure there will still be some headwinds but nothing that wasn’t expected anyway.

The UK can now be an economic speedboat, now having many new and large trade deals agreed with countries we weren’t allowed to before. And having the continued and important strong relations with the European Union.

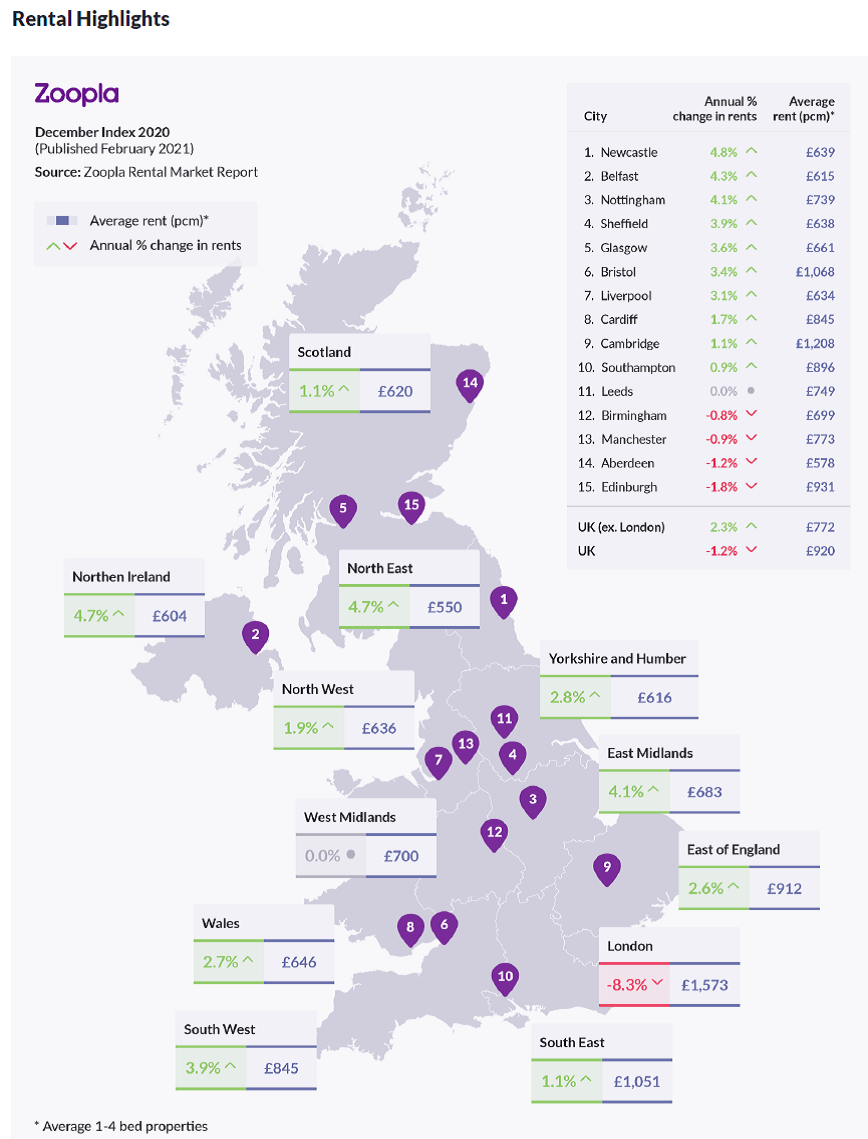

UK Rental Market Overview

Annual UK rental growth increases outside London

Average rents across the UK excluding London rose by 1.4% in the three months to the end of December, taking the annual growth in rents to 2.3%.

This compares to rental growth of 1.6% seen at the end of Q3 last year.

Rents are rising year-on-year in most regions across the UK, with the exception of the

West Midlands (0%) and London.

Demand and supply

Across the UK, demand for rental property is still rising, with total demand from renters in January some 21% higher than the same month last year.

At the same time, the supply of homes to let is more constrained, falling by 11% over the same period, and putting upward pressure on rents in many areas.

Demand in some well-connected towns across the country is putting particular upwards pressure on rents, with rental growth of more than 7%.

This trend is reversed in London, as rental supply outpaces demand, as more stock continues to come back to the market amid the changing working, commuting, tourism and business travel trends prompted by the COVID-19 pandemic and subsequent lockdowns.

Market Outlook

The pandemic has disrupted some of the key drivers of demand in the rental market – including labour mobility, migration and employment growth.

Despite this, we have seen a rise in localised demand in some areas, as some renters

look to relocate.

The outlook for the rental market, especially in central cities, will depend on how quickly the COVID-19 vaccine is rolled out, and how quickly it can start to have an effect and kick-start a return to more mobility across the country, and internationally.

As this happens, ‘business as usual’ will start to resume in city centres as business activity starts to rise, from the reopening of retail and offices to events spaces, leisure and entertainment facilities.

This will likely result in pick-up in demand in city centres, as well as a shift from long-term lets back to short-term lets in some cases, helping to absorb some rental stock - particularly in London.

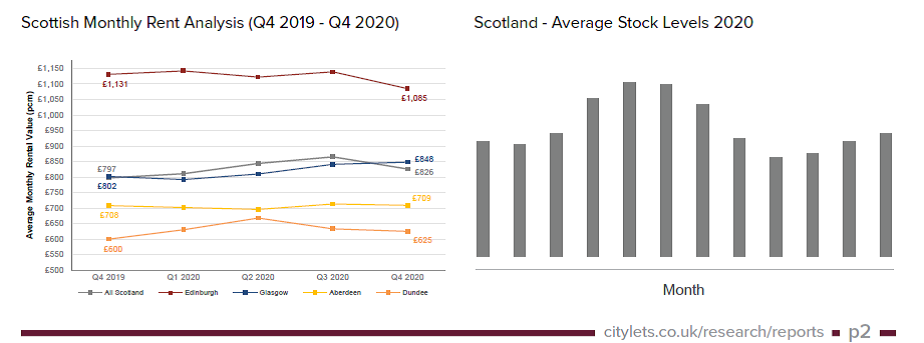

Scotland Rental Market.

Rental property search remained buoyant in Q4 2020 as Scotland moved onto a tiered approach to the coronavirus restrictions.

Property to rent in Scotland, on average, rose 3.6 % over the quarter to stand at £826 per month, less than the 5.4% reported in the previous quarter with material drag now exerted by falling rents in Edinburgh for the first time.

Closure of short term holiday rentals in particular saw the capital record a significant annualised fall at minus 4.1%.

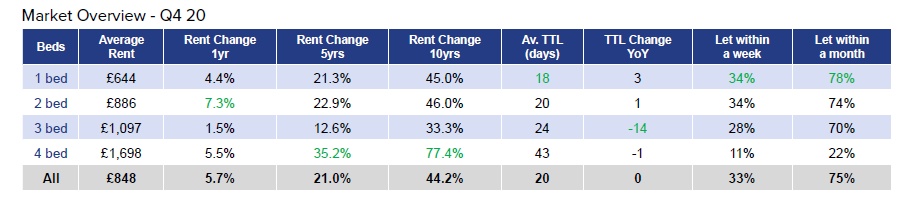

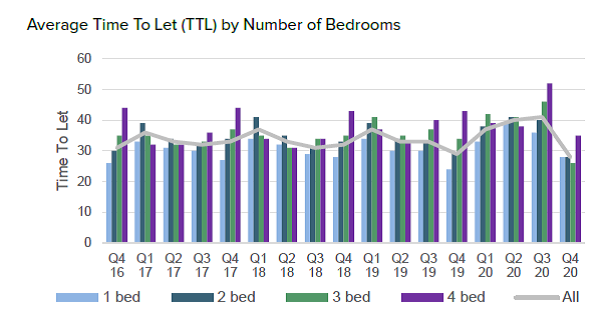

Glasgow Rental Market

Once again Glasgow and surrounding Local Authority regions posted the largest year on year rises

Rents in Glasgow rose 5.7% to stand at £848 on average with a TTL of just 20 days.

75% of properties to rent in Glasgow let within a month.

The reported figures for the Greater Glasgow region add further countenance to conjecture that the pandemic was leading to widespread exodus from cities.

Summary

The sales and rental market in Glasgow remains very buoyant and demand remains high at all levels of the market, compared to other parts of Scotland and the UK, as highlighted in the report information shown.

We certainly expect the strong BTL rental market demand to continue and strengthen without a doubt.

As house prices have risen and social housing supply remains constrained, the number of households in the private rented sector has doubled since 2001, rising from 2.3 million to 5.4 million by 2014.

That trend is continuing and there will be an additional 1.8 million in the private rented sector by 2025.

That would take the total to 7.2 million households in the UK rented.

That is about 25% and rising.

That is why our unique Social Housing Investment Opportunity (click to open) captures the market demand in Glasgow and is an easy, safe and secure strategy for all investors

And remember…..

- We want to take you to the next level in property investment

- We are here to help you take that step

- We are here as your second mentors

- We are always here for you and build a long term relationship

- We are here to Make a Difference for you.